How Credit Score Works: Complete Guide for Beginners (2025)

Understanding how credit score works is one of the most important steps to building a strong financial life. A credit score decides whether you get a loan, what interest rate you receive, and how easily you can access financial products like credit cards, home loans, EMI options, and even Buy Now Pay Later (BNPL) services.

In 2025, every bank, NBFC, and fintech lender checks your credit score before giving you any credit. If you know how credit score works, you can build a high score and unlock better financial opportunities.

This detailed beginner-friendly guide will help you understand:

- What a credit score is

- How credit score works step-by-step

- How banks calculate credit score

- Factors influencing your credit score

- How to improve your credit score fast

- Common myths about credit scores

- Why scores drop suddenly

- Credit score ranges and meanings

- How to check your credit score for free

- Best practices to maintain a high score

Let’s dive deep and understand everything in simple terms.

What Is a Credit Score? (And How Credit Score Works?)

A credit score is a 3-digit number between 300 and 900 that represents your creditworthiness — how reliable you are at repaying borrowed money. Higher score means lenders trust you more. Lower score means high-risk borrower.

When understanding how credit score works, remember this:

Your credit score is a reflection of how responsibly you handle loans, EMIs, and credit cards.

In India, four major bureaus calculate your score:

- CIBIL

- Experian

- Equifax

- CRIF Highmark

They track your entire credit history and calculate your score using multiple factors.

Credit Score Range (Table)

| Credit Score | Rating | Meaning |

|---|---|---|

| 300–549 | Very Poor | High risk, loan rejection likely |

| 550–649 | Poor | Difficult to get loans |

| 650–699 | Fair | Average approval probability |

| 700–749 | Good | Good approval rate |

| 750–900 | Excellent | Instant loans, low interest rates |

A score above 750 is ideal for credit cards and personal loans.

Why Credit Score Matters?

Understanding how credit score works is extremely important because your credit score directly affects almost every part of your financial life. Whether you apply for a personal loan, credit card, home loan, or even a small EMI plan, lenders rely on your score to decide if you are a safe borrower. A good score increases your financial freedom, while a poor score limits your opportunities.

✔ 1. Loan Approval

Banks and NBFCs first check your credit score before approving any loan. If you know how credit score works, you’ll understand that lenders give priority to borrowers with a high score because they are considered low-risk. A score above 750 improves your chances of getting personal loans, car loans, and home loans without any hassle. A low score often leads to loan rejection or strict verification.

✔ 2. Lower Interest Rates

Your credit score not only affects loan approval but also determines the interest rate you receive. When you understand how credit score works, you’ll see that lenders reward high-score customers with reduced interest rates because they trust them more. Even a small difference in interest rate can save you thousands or lakhs over long-term loans like home loans or car loans.

✔ 3. Credit Card Eligibility

Most premium and high-limit credit cards require a strong credit score. Knowing how credit score works helps you qualify for cashback cards, reward cards, airport lounge cards, and premium travel credit cards. A poor score limits your options to basic or secured cards.

✔ 4. Higher Credit Limits

Credit Score also decides your credit card limit. When you maintain a good score and show responsible usage, banks automatically offer credit limit increases. This is another reason why understanding how credit score works is important—it helps you gain more purchasing power and better credit flexibility.

✔ 5. Pre-Approved Loans

Many banks offer pre-approved personal loans and instant credit card approvals only to people with high credit scores. When you truly understand how credit score works, you can maintain a score that qualifies you for these quick, zero-paperwork financial products. These offers save time and provide instant access to money when needed.

✔ 6. Better Negotiation Power

With a high credit score, you can negotiate better loan terms, lower processing fees, and flexible repayment options. This advantage comes only when you know how credit score works and maintain the score consistently.

✔ 7. Helps in Renting Homes or Applying for Jobs

Some companies and landlords check credit scores before giving rental property or approving job applications in the finance sector. A good understanding of how credit score works ensures you maintain a clean financial profile that boosts your credibility.

✔ 8. Strong Financial Reputation

A high credit score reflects financial discipline. It builds trust with lenders, increases your financial stability, and prepares you for future goals like buying a house, car, or starting a business. Understanding how credit score works helps you maintain a strong financial reputation throughout your life.

How Credit Score Works: Step-by-Step Explanation

Let’s simplify how credit score works in a simple and practical way.

1. You Take a Loan or Credit Card

Understanding how credit score works becomes easier when you look at what happens the moment you borrow money or use credit. Whenever you apply for or start using any type of credit, your financial activity gets recorded by the lender. This includes:

- Personal loan

- Home loan

- Car loan

- Credit card

- BNPL services like ZestMoney, LazyPay, PayLater, Slice, etc.

The moment you take any of these credit products, the bank or lender begins tracking how you handle the borrowed money. Every EMI you pay, every credit card bill you clear, and every delay you make becomes part of your credit history. This is the first and most important step in understanding how credit score works, because your behaviour from this point forward shapes your future score.

Banks carefully monitor:

- Whether you pay on time

- Whether you delay payments

- Whether your EMI bounces

- Whether you use credit responsibly

- Whether you take too many loans

This initial record is the foundation of your credit profile. If you know how credit score works, you’ll see that even small financial actions—paying bills late, maxing out credit cards, or missing an EMI—can impact your score for months or even years. So the moment you start using credit, your credit journey officially begins, and every step is reported to credit bureaus like CIBIL, Experian, CRIF, and Equifax.

2. Bank Reports Your Activity to Credit Bureaus

To understand how credit score works, this step is extremely important. After you take a loan or start using a credit card, your bank or lending company doesn’t just track your behaviour — they also report it to the major credit bureaus. Every month, without fail, lenders send detailed updates about your credit activity to CIBIL, Experian, Equifax, and CRIF Highmark.

These reports include:

- Whether your EMI was paid or missed

- Whether your credit card bill was paid in full, paid partially, or left pending

- How much of your credit limit you used (credit utilisation)

- Whether you have overdue loans

- Details of any new loans you take

- Information on loans you close

- Any defaults, late payments, or settlements

All this information becomes part of your credit history.

This process is the backbone of how credit score works, because credit bureaus rely completely on this monthly data to calculate your score. Even a single delayed EMI or a high credit usage in one month can bring down your score when the lender submits the update.

Banks don’t judge you emotionally — they rely on numbers.

Whatever you do with your loans and credit cards is sent to bureaus as raw data, and that data directly affects your credit score.

So the more responsible your behaviour, the stronger your score becomes. The more mistakes you make, the more your score drops. This monthly reporting system is what keeps your credit score accurate and updated.

3. Bureaus Analyse Your Behaviour

Once lenders send your monthly data, the next step in understanding how credit score works is the analysis done by credit bureaus. CIBIL, Experian, Equifax, and CRIF Highmark carefully study your financial behaviour to determine how reliable you are as a borrower. They don’t just collect your information — they evaluate it using advanced algorithms and scoring models.

Here’s what credit bureaus check in detail:

✔ Do you pay your bills on time?

Your payment history is the single most important factor in understanding how credit score works. Bureaus analyse if your EMIs and credit card dues are paid before the due date or if you delay payments. Even one missed EMI can reduce your score significantly because it signals risk.

✔ Are you using too much credit?

They check how much of your credit limit you are using each month. This is called credit utilisation ratio. If you use more than 30–40% of your limit regularly, bureaus consider it high risk. Understanding how credit score works means knowing that high utilisation = lower score.

✔ Are you applying for too many loans?

If you apply for multiple loans or credit cards within a short time, bureaus treat it as credit hunger. Too many hard inquiries reduce your score. This is another key part of how credit score works — applying frequently shows financial desperation.

✔ How long have you been using credit?

Your credit age (length of credit history) plays a major role. Bureaus check how long your oldest credit account has been active. Longer history = more trust. A short history means bureaus don’t have enough data to judge your financial behaviour.

In summary, bureaus analyse your entire credit pattern, not just one or two actions. This deeper analysis helps them calculate a fair and accurate score based on how responsibly you manage credit. Understanding this step is essential if you truly want to master how credit score works.

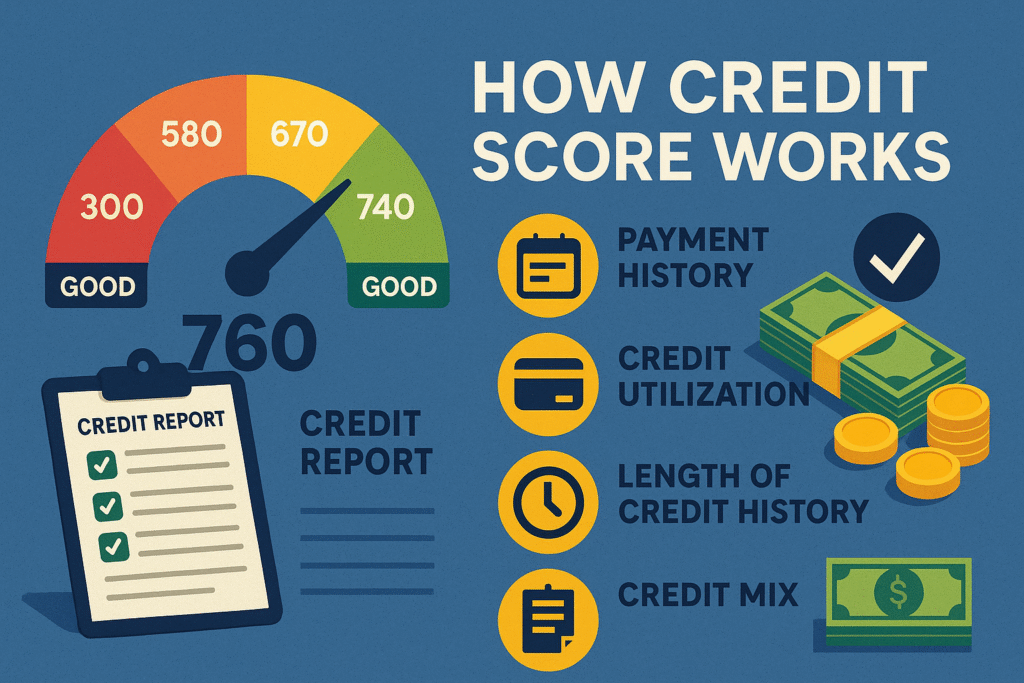

4. Score Calculation Formula Applies

Once the bureaus finish analysing your financial behaviour, the next step in understanding how credit score works is the actual calculation process. Your score isn’t decided randomly — it follows a strict mathematical formula used by all major credit bureaus like CIBIL, Experian, Equifax, and CRIF.

This formula assigns a specific percentage of weight to each part of your credit behaviour. Together, these factors determine whether your score should go up, stay stable, or drop.

Here is how credit score works mathematically:

• Payment History – 35% (Most Important Factor)

This is the largest and most influential component of your credit score. Credit bureaus check how consistently you pay your EMIs and credit card bills. Even a single missed payment can cause a 60–100 point drop. If you want to understand how credit score works, remember this:

Timely payments = strong score. Late payments = instant drop.

• Credit Utilisation – 30%

Credit utilisation tells bureaus how much of your credit limit you are using. If your card limit is ₹1,00,000 and you regularly use ₹70,000–₹100,000, bureaus see you as a high-risk borrower.

Understanding how credit score works means keeping utilisation below 30% to show responsible credit behaviour.

• Length of Credit History – 15%

This factor checks how long you’ve been using credit. Older credit accounts help build trust. A long credit history allows bureaus to evaluate your behaviour more accurately.

The longer your credit age, the better your score. This is why understanding how credit score works includes never closing your oldest card.

• Credit Mix – 10%

Your score improves when you use a healthy combination of both secured loans (home loan, car loan) and unsecured loans (credit card, personal loan).

A good mix shows lenders that you can handle different types of credit responsibly. This is a subtle but important part of how credit score works.

• Hard Inquiries – 10%

Every time you apply for a loan or credit card, lenders perform a hard enquiry on your profile. Multiple enquiries in a short time reduce your score.

This is why understanding how credit score works means avoiding unnecessary loan applications.

These five components together create your final credit score between 300 and 900. When you understand how each factor contributes, you gain the power to control and improve your score more effectively.

Credit Score Calculation: Detailed Breakdown

1. Payment History (35%)

Missing an EMI can drop your score by 60–100 points.

Includes:

- Loan EMIs

- Credit card payments

- BNPL due payments

TIP:

Always pay before due date.

2. Credit Utilisation Ratio (30%)

If your credit limit is ₹1,00,000, don’t use more than ₹30,000 (30%).

Using more than 50% shows risk.

3. Length of Credit History (15%)

If your oldest credit card is 8 years old, it boosts your score.

TIP:

Never close your oldest credit card.

4. Credit Mix (10%)

Banks prefer:

- Home loan / car loan (secured)

- Personal loan / credit card (unsecured)

A good mix improves score.

5. Hard Enquiries (10%)

Every time you apply for a loan, score reduces.

Limit applications.

Signs You Have Good Credit Management

You will know you understood how credit score works if:

- Your score stays above 750

- You pay all bills before due date

- You use credit card wisely

- You maintain low credit utilisation

- You avoid loan shopping

How to Improve Credit Score Fast in 2025

Below are the best ways to increase your credit score quickly and safely.

1. Always Pay EMIs and Credit Card Bills On Time

This is the #1 factor in how credit score works.

Use Auto-Pay.

2. Keep Credit Utilisation Below 30%

This improves your score in 30–60 days.

3. Increase Credit Limit

Call bank and request a limit increase.

4. Don’t Close Old Credit Cards

Old cards = long history = good score.

5. Avoid Too Many Loan Applications

Apply only when necessary.

6. Clear Credit Card Dues Fully

Don’t pay only minimum due.

7. Use a Small Secured Loan

Like:

- Gold loan

- FD-backed credit card

These boost score safely.

Common Myths About How Credit Score Works

❌ Myth 1: Checking credit score reduces it

✔ Truth: Only bank hard checks reduce score.

❌ Myth 2: No loan history = high score

✔ Truth: No credit → score cannot be calculated (“NA”).

❌ Myth 3: Paying minimum due is enough

✔ Truth: No, you must pay total amount.

❌ Myth 4: Closing loans quickly increases score

✔ Truth: Long repayment builds history.

Why Credit Score Drops Suddenly?

Reasons:

- Missed EMI

- High credit card usage

- Too many loan applications

- Closing old accounts

- Overdue BNPL payments

- Credit card settlement

- High number of inquiries

Credit Score vs Credit Report

| Feature | Credit Score | Credit Report |

|---|---|---|

| Type | Numeric | Detailed record |

| Range | 300–900 | No fixed range |

| Contains | Summary | Full history |

| Purpose | Quick check | Full evaluation |

How to Check Your Credit Score for Free

You can check at:

✔ Official Sites

✔ Banking Apps

- HDFC

- ICICI

- SBI

- Kotak

- Axis

Checking your score does NOT reduce it.

Ideal Credit Score Needed for Different Loans

| Loan Type | Ideal Score | Approval Chance |

|---|---|---|

| Personal Loan | 720+ | High |

| Credit Card | 700+ | Good |

| Home Loan | 750+ | Excellent |

| Car Loan | 700+ | Good |

| Business Loan | 750+ | High |

Best Practices to Maintain a Good Credit Score

- Pay bills early

- Use credit card smartly

- Keep utilisation low

- Avoid loan shopping

- Keep old credit lines active

- Review your credit report every 6 months

Internal Links (Add These in Your Blog)

(To satisfy RankMath)

- Read: Best Credit Cards for Beginners in 2025

- Read: How to Improve Credit Score in India

Insert links to your own posts.

External Links (Add These for RankMath)

(To increase authority)

- CIBIL: https://www.cibil.com

- RBI: https://www.rbi.org.in

- Experian: https://www.experian.in

Conclusion

Now you clearly understand how credit score works and how it affects your financial life. A good credit score helps you get faster loan approvals, lower interest rates, and premium credit cards. If you focus on timely payments, low credit usage, and responsible credit behaviour, your score will naturally stay above 750.

Check our other financial guide for beginners